Rental Income Tax Malaysia Public Ruling

2018 2019 malaysian tax booklet 17 public rulings and advance rulings to facilitate compliance with the law.

Rental income tax malaysia public ruling. In malaysia income derived from letting of real properties is taxable under paragraph 4 a business income or 4 d rental income of the income tax act 1967. Director general s public ruling section 138a of the income tax act 1967 ita provides that the director general is empowered to make a public ruling in relation to the application of any provisions of the ita. Deloitte tax hand information and insights from deloitte s tax specialists globally.

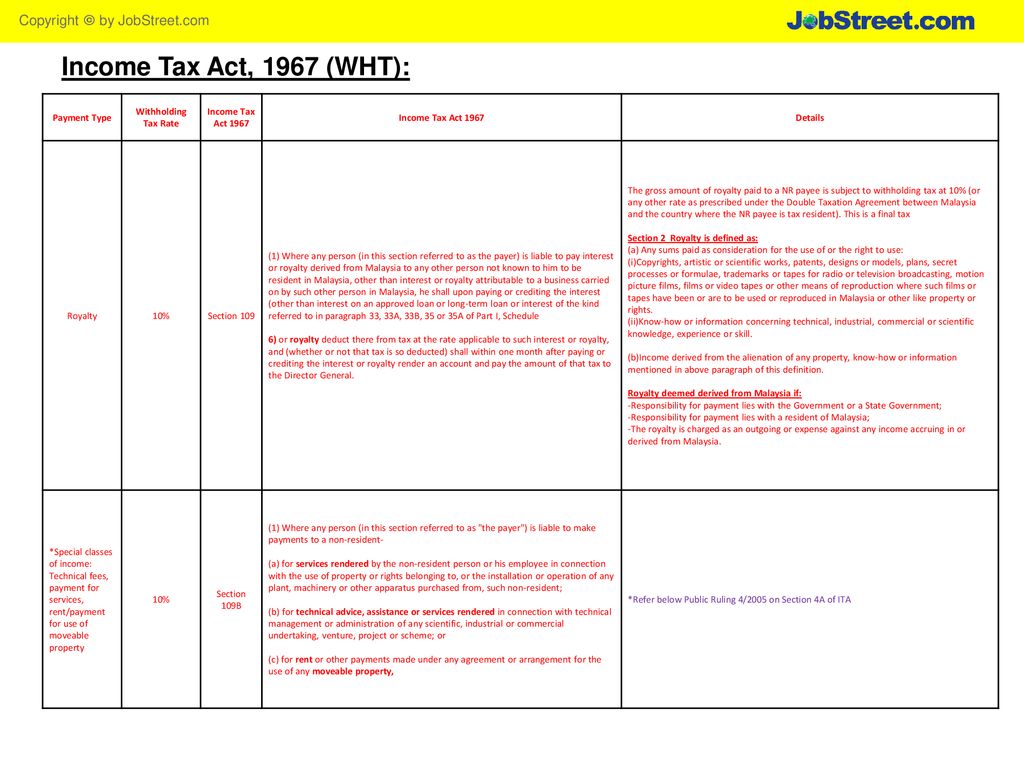

The inland revenue board irb of malaysia issued public ruling pr no. 1 2014 last amended on 27 june 2018. Remuneration or other income in respect of services performed or rendered in malaysia by a nr public entertainer is subject to withholding tax of 15 on the gross payment.

12 2018 inland revenue board of malaysia date of publication. 19 december 2018 1. A public ruling is published as a guide for the public and officers of the inland revenue board of malaysia.

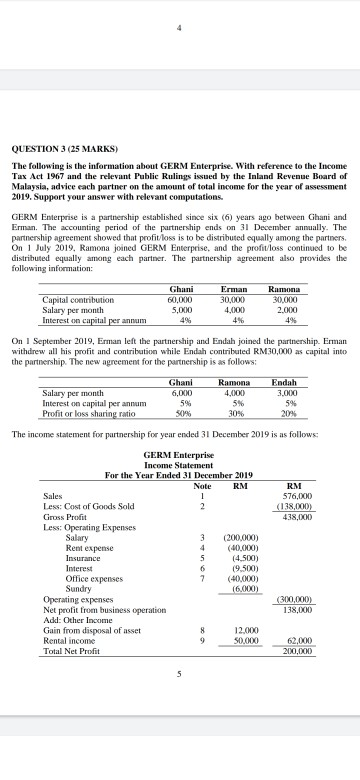

The income is deemed as a business sources if maintenance services or support services are comprehensively and actively provided in relation to the real property. Individuals who own property situated in malaysia and receive rental income in return are subject to income tax. Rental of moveable property.

Objective this public ruling pr explains. The definition of employment income covers all forms of remuneration including benefits whether in cash or in kind received by an individual for exercising or having an employment in malaysia 14 therefore an employee s income with respect to their employment in malaysia will be subject to malaysian tax regardless of whether it is paid in malaysia or outside malaysia. Rental income is.

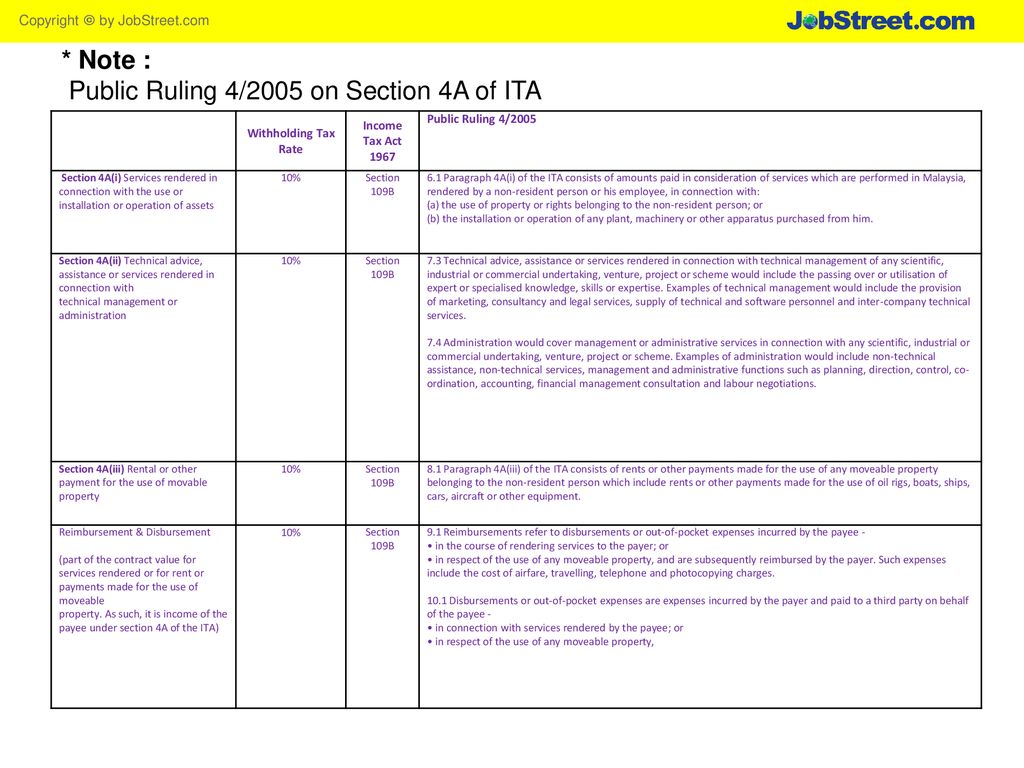

Special classes of income. And b letting of real property as a non business source under paragraph 4 d of the ita. Income tax in malaysia is imposed on income accruing in or derived from malaysia except.

Sponsor of the nr public entertainer is required to pay withholding tax of 15 before an entry permit for the nr public entertainer can be obtained from the immigration department. Such rental income is explained under section 4 d of the act. A public ruling as provided for under section 138a of the income tax act 1967 is issued for the purpose of providing guidance for the public and officers of the inland revenue board malaysia.